FASB Proposes Not-for-Profit Accounting Standards Update

The Financial Accounting Standards Board (FASB) recently proposed an accounting standards update (ASU) for not-for-profit entities. The proposed update will affect not-for-profit organizations (topic 958) and health care entities (topic 954), and is designed to make financial statements more useful.

FASB shared this statement in a press release on the topic:

- “The proposed ASU contains recommended enhancements to the fundamental reporting model for not-for-profit organizations-a model that has existed for more than 20 years,” stated FASB member Lawrence W. Smith. “We believe that these changes will refresh the model in ways that will make not-for-profit financial statements even more useful to donors, lenders, and other users.”

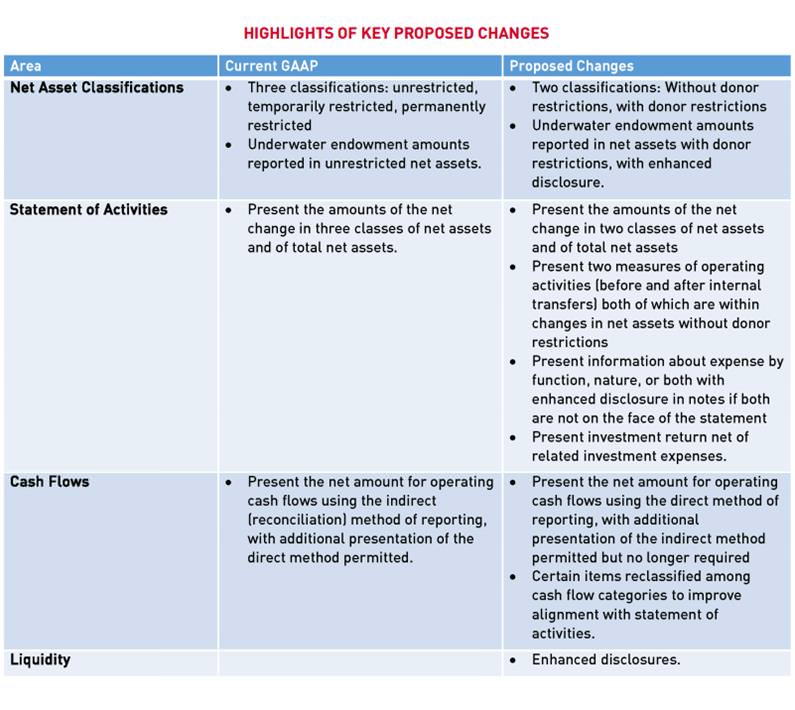

The proposal, Project: 2015-230 Presentation of Financial Statements of Not-for-Profit Entities, includes major changes to the following reporting areas:

- Net asset classification

- Liquidity

- Statement of activities

- Cash flows

FASB is accepting public comments on the proposal through Aug. 20, 2015, which can be submitted here.

The standards board recently held an educational webcast outlining the objectives of the proposal, key improvements that will take place if adopted and rationale behind the updates. The webcast is available for viewing here (you must register to access the archived event).

Whalen & Company will stay on top of the progress of this exposure draft proposal and we will keep our not-for-profit clients apprised of changes to reporting standards. An effective date will be determined by the FASB once they have considered all comments and feedback received from third parties. It is expected, however, that all amendments proposed in the ASU would be applied on a retrospective basis. In the first year of application, a not-for-profit entity would be required to disclose the nature of any re-classifications or restatements and their effects, if any, on changes in the net asset classes for each year presented.

Links to Key Resources for FASB’s Proposed Accounting Standards Update:

- FASB In Focus: Overview of Proposed Changes

- Full FASB 2015-230 Exposure Draft

- Public Comment form for 2015-230 Exposure Draft

- Educational Webcast Archive (you must register to launch the presentation)

If you have questions about FASB’s proposed updates to not-for-profit financial statement reporting, please contact your Whalen representative