Fronted Client Costs are CAT Taxable!

Written by: Steve Estelle

Applicable To: Consultants who front client costs

In mid-March, the Ohio Tax Department assessed Commercial Activity Tax (CAT) on reimbursed costs a law firm allegedly fronted on behalf of clients, but it didn’t assess tax on all such costs.

In mid-March, the Ohio Tax Department assessed Commercial Activity Tax (CAT) on reimbursed costs a law firm allegedly fronted on behalf of clients, but it didn’t assess tax on all such costs.

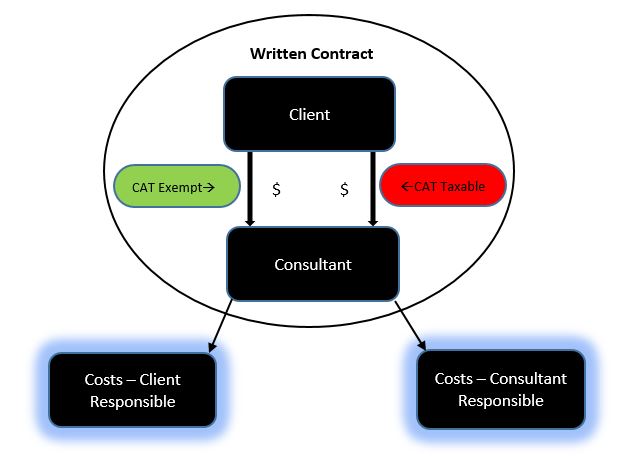

The conceptual difference between the taxable and exempt costs, the Department stated, was the taxable ones were “part of the price” of the firm’s “overall package of services,” and the others were not. The practical issue was which costs were included in the firm’s fee.

In general, CAT is owed on gross receipts but not on an agent’s receipts from its principal that the agent is to forward to a third party (i.e., when the agent acts as a conduit). R.C. 5751.01(F)(2)(l).

Taxable Costs – The engagement contracts between the firm and its clients didn’t appear to delineate who was responsible for these costs. Also, there were no separate service agreements identifying the firm as an agent for the client for these costs. Either would have been evidence that the firm was acting as an agent when it paid the costs.

Due to this silence, a presumption arose under O.A.C. 5703-29-13(C)(2)(a) that the firm wasn’t acting as an agent (i.e., the firm was responsible for the costs). There was no other evidence or pattern of behavior that persuaded the Department otherwise.

In addition, the basic test for agency is whether the principal has control over the work of the agent, and the Department concluded the firm’s clients didn’t have control over how the firm performed its legal work. It also reiterated that exemptions are strictly construed against the taxpayer.

Exempt Costs – The Department appeared to rely solely on division (E) of the above-cited regulation which exempts reimbursements for “fees [paid] on behalf of a client.” The exempt costs all appeared to be governmental fees. To name a few:

- Articles of Incorporation fees,

- UCC filing fees,

- Probate fees,

- Court costs, etc.

In contrast, the taxable costs were all for service providers, such as consultants, local counsel, experts, investigators, court reporters, mediators, translators, etc.

Next Step – Determine whether you’re reporting expense reimbursements as taxable CAT gross receipts. If not, contact Steve for further information.